Capital Gain Bonds

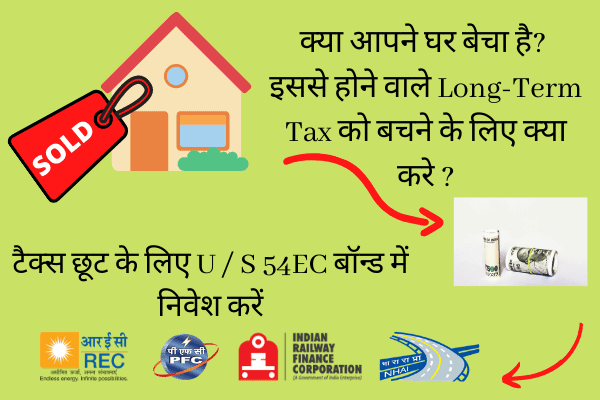

When a taxpayer sells long-term immovable property (land or building), they have the option to avail capital gain exemption under Section 54EC by investing in certain bonds.

Section 54EC bonds, also known as Capital gain bonds are fixed income instruments which provide capital gains tax exemption under section 54EC to the investors.

To be eligible for exemption under Section 54EC, the taxpayer must meet the following conditions:

- The exemption under Section 54EC can be claimed by any taxpayer, including individuals, Hindu Undivided Families (HUFs), companies, LLPs, firms, and others.

- The asset being sold should be a Long Term Capital Asset, which includes land or building or both. The asset is considered long-term if the taxpayer has held it for a minimum of 24 months prior to the sale.

- The taxpayer must invest the Capital Gains within 6 months from the date of transfer.

- The investment should be made in 54EC bonds: National Highways Authority of India (NHAI), Rural Electrification Corporation (REC), Power Finance Corporation Limited (PFC) bonds, or Indian Railway Finance Corporation (IRFC) Limited bonds.

- The total investment amount cannot exceed INR 50 lakhs during the current financial year and the subsequent financial year.

BONDS ELIGIBLE FOR EXEMPTION UNDER SECTION 54EC OF INCOME TAX ACT

BONDS ELIGIBLE FOR EXEMPTION UNDER SECTION 54EC OF INCOME TAX ACT

- Rural Electrification Corporation Limited or REC bonds,

- National Highway Authority of India or NHAI bonds,

- Power Finance Corporation Limited or PFC bonds,

- Indian Railway Finance Corporation Limited or IRFC bonds.

KEY FACTS TO AVAIL LTCG EXEMPTION BY INVESTMENT IN CAPITAL GAIN BONDS

KEY FACTS TO AVAIL LTCG EXEMPTION BY INVESTMENT IN CAPITAL GAIN BONDS

- To avail the tax-exemption the investment must be made within 6 months of the date of sale of immovable property.

- Such investment can be redeemed only after 5 years. Before april 2018 the bonds could be redeemed within 3 years.

- The exemption on investment is allowed only against long term capital gains on sale of immovable property (i.e. sale of land or building).

- The exemption is available up to a maximum amount of Rs 50 lakh